What is a Assurance Vie

A Complete Guide to France’s Most Popular Investment

If you’re living in France as an expatriate, one of the most effective ways to grow your wealth, reduce tax on investment gains, and plan for succession is through an Assurance Vie.

Often mistaken for a simple life insurance policy, the French Assurance Vie is actually a highly flexible, tax-efficient investment wrapper. It’s widely used by both French residents and international investors for long-term wealth accumulation, retirement planning, and inheritance optimisation. When structured correctly, it can significantly improve your tax position and give you greater control over how your assets are passed on.

What Is an Assurance Vie?

An Assurance Vie is a long-term investment issued by a European life company. You can contribute a lump sum or regular payments and invest across a wide range of assets — from capital-guaranteed euro funds to global equities, bonds, and diversified managed portfolios.

Although it includes a life insurance element, its primary purpose is not life cover. Instead, it’s designed to provide tax-advantaged investment growth and flexible wealth management, all within a structure that simplifies estate planning.

Key Tax Advantages

Example Withdrawals — How the Tax Works

To illustrate, here are two simple examples showing how withdrawals are taxed after eight years.

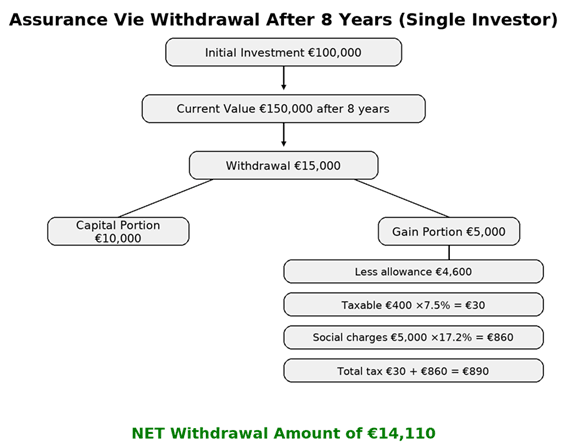

Example 1 – Single investor (John)

John invests €100,000 into an Assurance Vie. After eight years, the policy has grown to €150,000 (a €50,000 gain).

He withdraws €15,000. The gain portion of that withdrawal is €5,000.

After the annual €4,600 allowance, only €400 of gain is taxable at 7.5%, while social charges of 17.2% apply to the full gain.

- Income tax: €400 × 7.5 % = €30

- Social charges: €5,000 × 17.2 % = €860

- Total tax: €30 + €860 = €890

- Net received: €14,110

- Effective tax rate on the €15,000 withdrawal ≈ 5.9 %

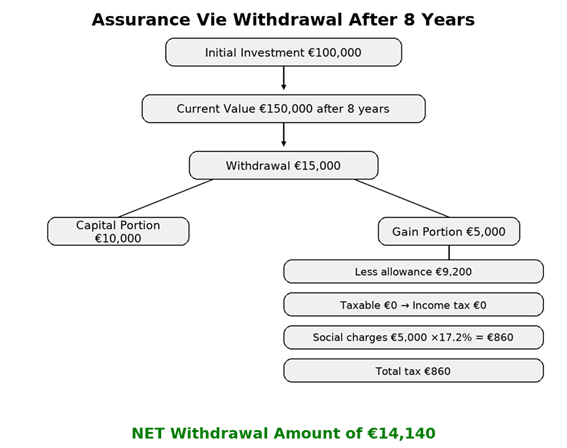

Example 2 – Joint policy (John & Linda)

If the policy is held jointly, the couple benefits from the higher €9,200 allowance.

The €5,000 gain in their €15,000 withdrawal is fully covered by the allowance, so no income tax applies — only social charges.

- Income tax: €0

- Social charges: €5,000 × 17.2 % = €860

- Total tax: €860

- Net received: €14,140

- Effective tax rate on the €15,000 withdrawal ≈ 5.7 %

Key takeaway: After eight years, the PFU rate falls to 7.5% on most investments, and the annual allowance can significantly reduce or even eliminate the income tax portion. For couples, this can often remove the income tax element altogether. However, if total premiums exceed €150,000, gains linked to the excess are taxed at 12.8% instead of 7.5%.

How Expats Typically Use Assurance Vie’s

Investment Performance & Options

Your returns depend on the underlying funds selected. Many expats choose risk-rated managed portfolios (e.g. balanced or growth strategies), while others prefer capital-protected euro funds for greater stability.

Both active and passive investment options are available, and you can switch or rebalance your investments at any time without triggering taxation.

This flexibility allows your portfolio to adapt as your circumstances evolve.

Why It Beats Traditional Bank Savings

Standard French bank accounts (Livret A, term deposits, etc.) offer low returns and limited planning flexibility. An Assurance Vie provides:

Choosing the Right Investment

Not all Assurance Vie plans are the same. Key things to look for:

- Clear, transparent fees.

- English-language reporting & support.

- Wide investment choice — multi-asset funds, ETFs, active or passive strategies.

- Flexibility to change beneficiaries, withdrawals, or currency.

French retail bank versions often have limited fund ranges, less flexibility, and higher fees. International versions generally offer better investment access, service, and investor protection.

For a closer look at one of the most popular expat-focused options, read my Prudential Assurance Vie France review — a detailed guide on performance, tax treatment, and why it’s one of the best Assurance Vie solutions for expats in France.

My Verdict

The Assurance Vie is one of the most effective financial planning tools for expatriates in France with £20,000/€25,000+ to invest. Its combination of tax deferral, reduced withdrawal tax after 8 years, and huge inheritance tax planning features makes it far superior to holding investments directly or leaving cash in banks or in UK products.

For expats, the ability to hold assets in multiple currencies and keep the same structure when moving abroad is especially valuable.

If you’re an expat in France looking to invest tax-efficiently and simplify succession, an Assurance Vie is almost always worth considering as part of your broader financial strategy.